Technological Evolution: The “Grabody” Roadmap

The company’s R&D strategy has evolved across three distinct generations of innovation.

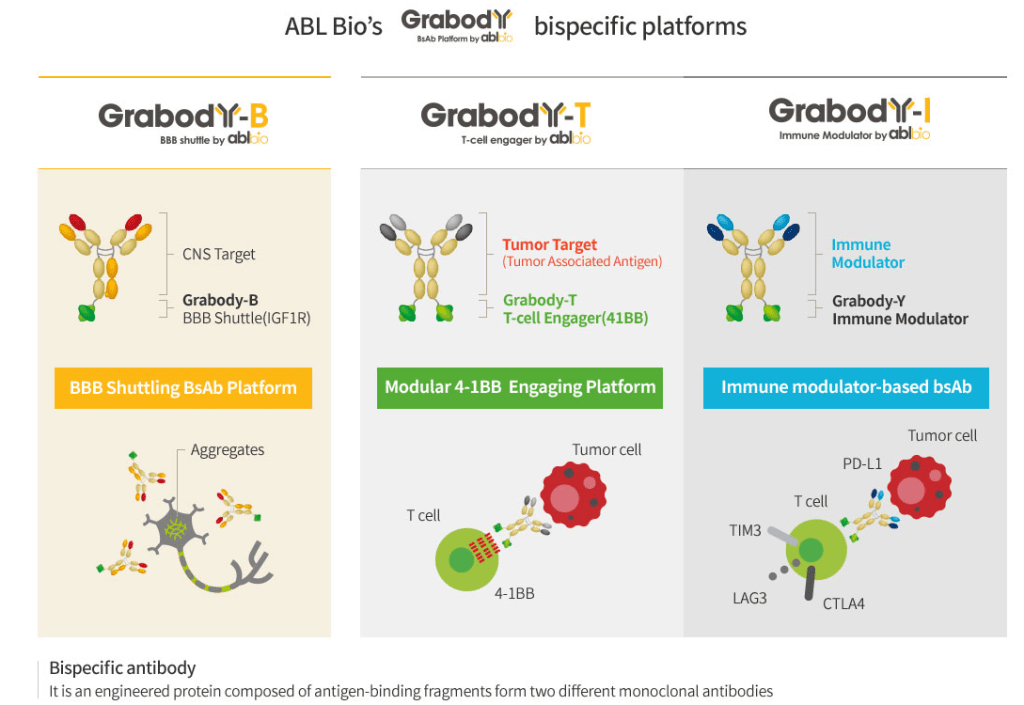

Phase 1: The “Grabody” Platform Foundation

Initial focus was on mastering Bispecific Antibodies, which target two different antigens simultaneously to increase efficacy and reduce toxicity.

- Grabody-T: A 4-1BB-based immuno-oncology platform designed to activate immune cells only within the tumor microenvironment, solving the chronic “liver toxicity” issues of previous 4-1BB therapies.

- Grabody-B: A “Blood-Brain Barrier (BBB) Shuttle” platform using IGF1R to deliver therapeutics across the notoriously difficult-to-penetrate BBB.

Phase 2: Global Validation of the BBB Shuttle (2022–2025)

The focus shifted to commercializing the BBB shuttle as a “platform-as-a-service” for Neurodegenerative diseases.

- The Sanofi Deal for Parkinson’s disease (ABL301) proved that ABL Bio’s shuttle technology is a world-class solution for delivering large molecules into the brain.

Phase 3: The Era of Bispecific ADCs (2026 & Beyond)

This is the current “frontier” for the company, combining the precision of bispecific antibodies with the potency of Antibody-Drug Conjugates (ADCs).

- Bispecific ADC (BsADC): Unlike standard ADCs, BsADCs (e.g., ABL206, ABL209) target two antigens on cancer cells, providing even higher selectivity and “killing power” while minimizing off-target side effects.

- NEOK Bio: ABL Bio established this U.S.-based subsidiary to lead global clinical trials for its BsADC pipeline, marking a shift from being a “technology licensor” to a “global drug developer.”

Reference: https://www.ablbio.com/en/company/platform

| Category | Key Insight |

|---|---|

| Core Momentum | FDA Phase 1 entry for next-gen Bispecific ADCs in 2026. |

| Financial Health | Strong cash reserves; transition to commercial royalty revenue expected by 2027. |

| Moat | Proprietary BBB Shuttle (Grabody-B) validated by Lilly, GSK, and Sanofi. |

| Strategic Goal | Becoming a top-tier global developer of ADC and CNS therapeutics. |

Financial Analysis: Shifting to a Royalty-Driven Model (2026 Outlook)

ABL Bio has transitioned from a cash-burning R&D firm to a company with a visible path toward sustainable profitability.

- Strategic Licensing Milestone (2025-2026):

- GSK Deal (April 2025): A $3.1 billion (KRW 4.1 trillion) agreement for the Grabody-B platform.

- Eli Lilly Deal (Nov 2025): A $2.8 billion agreement including a $15 million equity investment, significantly strengthening the balance sheet.

- Revenue Transformation: * Cash Runway: Massive upfront payments from 2025 deals have secured an R&D “runway” through 2028.

- Royalty Inflection Point: As lead assets like ABL001 enter late-stage clinical trials, the company is projected to begin receiving commercial royalties by 2027, fundamentally altering its earnings quality.

- Market Position: As of January 2026, its market capitalization exceeds KRW 10 trillion, solidifying its status as a “blue-chip” K-Bio enterprise.

Analyzing the success of ABL Bio

“Platform-Based” Scalability

Instead of betting everything on a single drug candidate, ABL Bio developed versatile platforms (Grabody). This “Plug-and-Play” approach significantly lowered risk:

- The “Shuttle” Advantage: Their Grabody-B (BBB Shuttle) solved a massive industry bottleneck: delivering drugs to the brain. Because this is a platform, it can be attached to various internal and external drug candidates, creating multiple revenue streams from a single technology.

- De-risking through Platforms: Even if one specific drug fails in trials, the underlying platform technology remains valid and sellable to other partners.

“Early-Stage L/O” Strategy

ABL Bio mastered the “Early Licensing-Out” model to ensure financial survival and validation.

- Quick Validation: By licensing out assets at the Pre-clinical or Phase 1 stage to giants like Sanofi and GSK, they didn’t just earn “upfront payments”— they earned “Global Proof of Concept (PoC).”

- The Virtuous Cycle: The capital gained from early deals was immediately reinvested into higher-value technologies like Bispecific ADCs, allowing them to stay 2-3 years ahead of competitors.

Agility in “Modality Expansion”

A key secret to their longevity is their ability to pivot toward the “Next Big Thing” before the market becomes saturated.

- Standard Bispecifics → BBB Shuttles → Bispecific ADCs: They didn’t settle for being just a “Bispecific Antibody” company. They recognized the global shift toward ADCs (Antibody-Drug Conjugates) early and merged it with their bispecific expertise to create a higher-entry-barrier technology.

This is a premium valuation report for ABL Bio, integrating financial modeling (rNPV, EBITDA) with strategic analysis. This version is polished for an institutional investor audience.

Valuation Report: ABL Bio (2026.01.26)

From “Bio-Tech Dreams” to “Cash-Flow Reality”

As of January 26, 2026, ABL Bio is undergoing a fundamental re-rating. No longer valued merely on clinical “hope,” the company is now being appraised as a high-growth platform provider with tangible cash flows.

1. rNPV Analysis: Sum-of-the-Parts (SOTP) Valuation

The rNPV (Risk-adjusted Net Present Value) calculates the present value of future cash flows, adjusted for the Probability of Success (POS) at each clinical stage.

| Asset / Platform | Indication | Stage | Est. POS | rNPV Valuation |

| ABL301 (Sanofi) | Parkinson’s (BBB) | Phase 2 | 15–20% | ~$1.9B (KRW 2.5T) |

| Grabody-B Platform | CNS / Shuttle Tech | Licensing | 30% | ~$2.6B (KRW 3.5T) |

| ABL206/209 (BsADC) | Solid Tumors | Phase 1 | 10% | ~$1.5B (KRW 2.0T) |

| Grabody-T & Others | Immuno-Oncology | Various | 5–10% | ~$1.1B (KRW 1.5T) |

| Total Pipeline Value | ~$7.1B (KRW 9.5T) |

- Net Cash Position: Bolstered by 2025 milestones, the company holds approx. $0.7B–$0.8B in net cash.

- Implied Enterprise Value (EV): Approximately $7.8B–$8.2B (KRW 10.5T ~ 11T).

2. Technology-Driven EBITDA & Multiples

For platform companies, the EV/EBITDA metric becomes relevant once technology transfers trigger consistent upfronts and milestones.

- 2026 Est. Revenue: ~$340M (KRW 450B) — Driven by new L/O upfronts and progress milestones from GSK/Lilly.

- 2026 Est. EBITDA: ~$225M (KRW 300B) — Reflecting high margins typical of intellectual property (IP) licensing.

- Target Multiple: Global peers like Genmab or Halozyme trade at 30x–40x EBITDA during their scaling phase.

$225M (EBITDA) × 35 (Multiple) = ~$7.9B (KRW 10.6T)

3. Why the “Premium” is Justified: The “Tier-1 Supplier” Logic

The traditional “Bio-Venture” discount is disappearing for ABL Bio. Here’s why:

- Validation by Giants: Partnerships with Sanofi, GSK, and Eli Lilly act as a “Third-Party Audit.” Big Pharma’s capital injection confirms that the technology is not just viable, but essential.

- Scalability (The “Highway” Effect): The Grabody-B (BBB Shuttle) is a toll road. It doesn’t matter which “car” (drug) drives on it; ABL Bio collects the toll. This diversifies risk away from individual drug failures.

- The Rise of Bispecific ADCs: In 2026, ABL Bio is leading the next modality shift. By merging bispecific antibodies with ADCs, they have created a higher entry barrier that standard ADC companies cannot easily cross.

4. Strategic Conclusion

Current Market Cap (Jan 2026): Approx. KRW 10T+

Investment Verdict: Fair Value reached, but Momentum remains High.

While the current stock price reflects the established value of the BBB shuttle, the “Upside Surprise” now lies in the BsADC (Bispecific ADC) data. If the Phase 1 results for ABL206/209 demonstrate superior safety and efficacy over traditional ADCs, the market cap could comfortably break toward the KRW 15T mark as it begins to command a “Global Leader” premium.

Market Snapshot: ABL Bio [Jan 26, 2026]

댓글 남기기