The Shift from “First Mover” to “Smart Follower” and Innovation

In 2026, Samsung Bioepis is executing a dual-track strategy: stabilizing its massive biosimilar engine while navigating a more complex competitive landscape where “speed” is being challenged by “utility” (formulation).

1. Commercial Footprint: 11 Products and the “Direct Sales” Leap

As of early 2026, Samsung Bioepis has 11 biosimilars available in Europe, significantly expanding its direct control over the value chain.

- The Dual-Brand Launch (SB16): Samsung is currently directly selling OBODENCE™ (Prolia BS) and XBRYK™ (Xgeva BS) in Europe. This targets two multi-billion dollar markets (Endocrinology and Oncology) with the same molecule (denosumab), maximizing ROI.

- Ophthalmology Pivot: In Jan 2026, Samsung officially regained the European rights for BYOOVIZ™ (Lucentis BS) from Biogen. Combined with the UK launch of SB15 (Opuviz/Eylea BS) in Jan 2026, the company is now a dominant direct-selling force in European ophthalmology.

Full List of Samsung Bioepis Approved/Launched Products (Feb 2026)

Here is the finalized technical list of the 11 products currently driving the company’s valuation:

| # | Code | Reference Product | Brand Name (Example) | Therapeutic Area |

| 1 | SB4 | Enbrel | Benepali | Immunology |

| 2 | SB2 | Remicade | Flixabi | Immunology |

| 3 | SB5 | Humira | Imraldi / Hadlima | Immunology |

| 4 | SB3 | Herceptin | Ontruzant | Oncology |

| 5 | SB8 | Avastin | Aybintio | Oncology |

| 6 | SB11 | Lucentis | Byooviz | Ophthalmology |

| 7 | SB12 | Soliris | Epysqli | Hematology |

| 8 | SB17 | Stelara | Pyzchiva / Epyztek | Immunology |

| 9 | SB15 | Eylea | Opuviz / Apilivu | Ophthalmology |

| 10 | SB16 | Prolia | Obodence | Endocrinology |

| 11 | SB16 | Xgeva | Xbryk | Oncology (Supportive) |

* The 11th product is XBRYK™ (SB16), a biosimilar to Xgeva® (denosumab 120mg).

SB16 actually covers two distinct brands based on the reference drug’s indication:

- OBODENCE™ (SB16): Biosimilar to Prolia® (denosumab 60mg) — mainly for osteoporosis.

- XBRYK™ (SB16): Biosimilar to Xgeva® (denosumab 120mg) — mainly for bone metastases in oncology.

2. The SB27 (Keytruda BS) Challenge: IV vs. SC War

Samsung’s SB27 is in Phase 3, aiming for the massive “Keytruda Cliff” starting in 2028.

- The Formulation Trap: While Samsung is faster in the IV (Intravenous) development, the original maker (MSD) and competitors like Celltrion are focusing on SC (Subcutaneous) formulations.

- Technical Risk: Since patent expiration dates are fixed, Samsung’s “earlier” clinical finish may not translate to an earlier launch. If competitors launch an SC version shortly after Samsung’s IV version, the convenience of SC (2-5 min administration vs. 30+ min for IV) could render Samsung’s “first-mover” advantage in the IV segment less effective.

3. SBE303 & NexLab: Future De-risking

- SBE303 (Nectin-4 ADC): Secured FDA IND approval in Jan 2026. This is the company’s answer to the “post-biosimilar” era.

- NexLab’s Mission: To bridge the “SC gap.” NexLab is focusing on Peptide-based delivery tech to create proprietary long-acting and SC formulations that could protect future pipelines from the very “formulation risks” we see with SB27.

The “20 by 30” Strategy: Pivoting to a Global Biopharma Powerhouse

In 2026, Samsung Bioepis’ technical competitive edge is defined by “Industrialized Lifecycle Management” and its strategic expansion into Next-Generation Modalities (ADC).

Valuation Report: Samsung Bioepis (2026.02.01)

Transition to a “Cash-Flow First” Valuation Model

Following the JPM Healthcare Conference 2026, the market is valuing Samsung Bioepis based on its “20 by 30” roadmap (20 biosimilars by 2030) and its record-breaking KRW 1.67T revenue in 2025.

1. rNPV Analysis: Sum-of-the-Parts (SOTP)

| Asset / Segment | Products | Status | rNPV Valuation |

| Commercial Core | 11 Biosimilars (Humira, Lucentis, etc.) | Direct Sales Scaling | ~$10.4B (KRW 14.0T) |

| 2026 Growth Peak | SB15 (Eylea), SB16 (Prolia) | Global Launching Now | ~$3.7B (KRW 5.0T) |

| Future BS Pipeline | SB27 (Keytruda), Enhertu BS | Ph 1/3 & Early Dev | ~$1.38B (KRW 2.0T) |

| SBE303 (Novel ADC) | Nectin-4 ADC | Phase 1 Clinical | ~$0.4B (KRW 0.5T) |

| Epis NexLab & Tech | Delivery Tech (Peptide) | Early R&D | ~$0.1B (KRW 0.15T) |

| Total Pipeline Value | ~$15.98B (KRW 21.65T) |

Valuation Logic: Applied a conservative 30% discount to the SB27 pipeline to account for the “SC formulation risk” from rivals. Even with this, the total value remains significantly above the current market capitalization, indicating an undervaluation.

Analyst Adjustment:

- SBE303 (KRW 0.5T): Given the 10-15% success rate for first-in-human trials, 500B KRW reflects the asset’s risk-adjusted value.

- NexLab (KRW 0.15T): Valued as a “strategic asset” rather than a revenue center.

2. Financial Performance: The Profitability Breakout

- 2025 Actual Revenue: KRW 1.672T (Highest in history).

- 2026 Est. EBITDA: ~$385M (KRW 520B) — Margins are expanding as direct-to-market sales for ophthalmology (Eylea/Lucentis) and bone-health (Prolia) products begin in earnest.

- Valuation Multiple: A 25x EV/EBITDA multiple is applied, reflecting the company’s hybrid nature as a stable manufacturer with “Smart Bomb” (ADC) upside.

3. Why the “Premium” is Justified: The End-to-End Advantage

- The “Keytruda Cliff” Advantage: With SB27 (Keytruda BS) already in Phase 3, Samsung Bioepis is one of only 3 global players with the capacity to meet the massive demand when Keytruda loses exclusivity.

- Regulatory Speed: Samsung remains the gold standard for “First-Mover” speed. Their ability to secure a European settlement for Eylea just days ago (Jan 30) proves their legal and regulatory dominance.

- Low Capital Risk: While other biotechs struggle for funding, Bioepis uses its KRW 1.6T revenue to self-fund SBE303 and NexLab. This makes the “innovation” side essentially a “free option” for long-term investors.

4. Investment Rating: Accumulate

While the “Strong Buy” is reserved until an SC formulation strategy is confirmed, the current market price is an attractive entry point.

- Why Accumulate?

- The Cash Floor: With 11 products and expanding direct sales, the company generates sufficient EBITDA to fund its own R&D without shareholder dilution.

- Valuation Gap: At the current market price, the market is essentially valuing only the legacy biosimilars, giving zero value to the upcoming Eylea/Prolia windfall and the ADC pipeline.

- Stability Premium: Unlike “high-risk” pure-play biotechs, Samsung Bioepis offers a lower risk profile with “manufactured” success rates.

5. Strategic Conclusion

Market Verdict: “Underpriced Execution”

Samsung Bioepis is currently undervalued due to temporary accounting expenses and the market’s obsession with its rivals’ SC formulations. However, the sheer volume of its 11-product portfolio and its dominance in the IV oncology and ophthalmology markets provide a massive “Safety Margin.”

Final Conclusion:

“Investors should adopt a conservative but proactive Accumulate strategy. While the formulation battle for Keytruda is a real threat, the company’s ability to generate cash from its 11 validated products provides a solid floor. The gap between the KRW 21.6T NPV and the current market price will likely close as direct sales results materialize in H2 2026.”

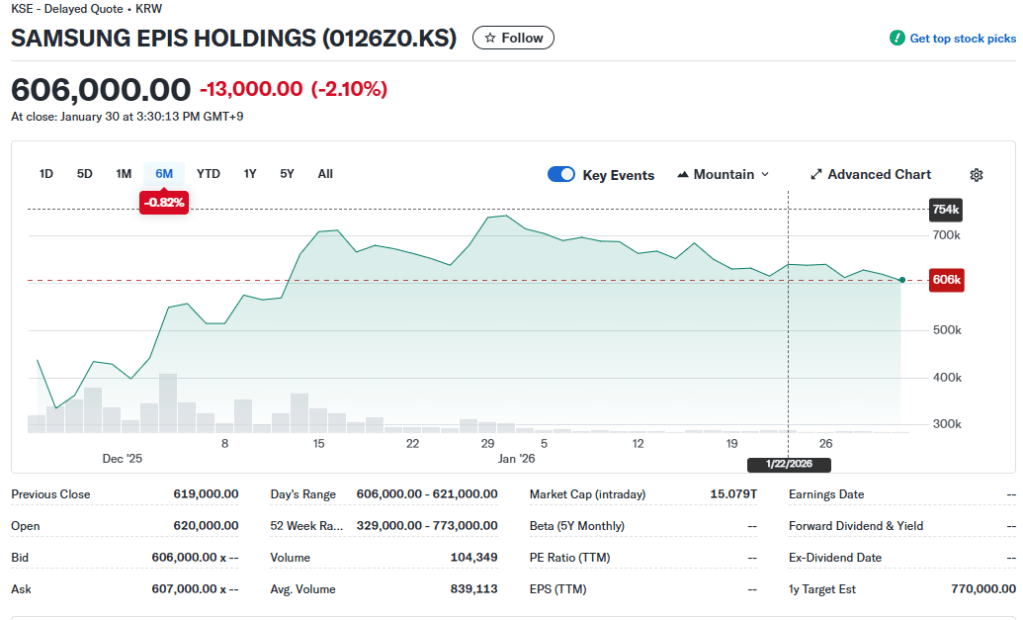

Market Snapshot: Samsung Epis Holdings [Feb 01, 2026]

(Additional) Why the “Market Gap” Persists in SAMSUNG EPIS HOLDINGS (Market Price vs. Value)

Technical Perspective:

The gap between the current stock price KRW 15.1T and KRW 21.6T valuation persists because investors are asking: “Will anyone want an IV biosimilar in a world dominated by SC originals?”

- The Patent Sync Problem: Patent expiration dates are fixed. Even if Samsung finishes trials 6 months early, it must wait for the patent to expire. This gives competitors (Celltrion, etc.) time to catch up and launch their SC versions almost simultaneously, negating Samsung’s clinical speed.

- Cost vs. Convenience: If Samsung cannot provide a massive price discount to offset the inconvenience of IV administration, its market share in the US/EU will likely be capped.

Financial Perspective:

The “undervaluation gap” identified is a classic case of accounting distortion vs. economic reality.

In the case of Samsung Bioepis (Samsung Epis Holdings), the financial friction stems from the legacy of its spin-off from Samsung Biologics and the specific way its “future value” is recorded on the balance sheet today.

1. The PPA Amortization “Paper Loss” (Accounting vs. Cash)

The most significant financial drag on the stock price is PPA (Purchase Price Allocation) Amortization.

- The Mechanism: When Samsung Biologics fully acquired Bioepis (and later spun it off), the “future potential” of drug pipelines (like SB27) was recorded as Intangible Assets. By law, these must be “depreciated” (amortized) over 10+ years.

- The Distortion: As of early 2026, this results in an annual non-cash expense of KRW 200B – 300B.

- Market Impact: While this has zero impact on actual cash flow, it slashes the “Net Income” shown on the income statement. Many automated trading algorithms and conservative retail investors see a “low net profit” and assume the stock is expensive, even though the EBITDA (Cash-based profit) is skyrocketing.

2. The “Holding Company Discount” & Liquidity Gap

Because Samsung Bioepis is now under Samsung Epis Holdings, it faces the “Korea Discount” typical of holding companies.

- Valuation Friction: Investors often apply a 20-30% discount to holding companies to account for potential double-taxation or management opacity.

- Supply/Demand (Flows): Since the 2025 spin-off, the stock has faced a “supply overhang.” Passive index funds (KOSPI 200) had to rebalance their portfolios, creating a period where there were more sellers than buyers regardless of the company’s actual performance.

3. Milestone Revenue Volatility

Samsung Bioepis is currently transitioning its financial DNA:

- Old Model: High reliance on one-time Milestone Payments from partners (Biogen, Organon). This made profits look “spiky” and unpredictable.

- New Model: Steady, high-margin Product Sales from direct commercialization (e.g., Byooviz, SB16).

- The “Gap” Reason: During this transition, the loss of large milestones can make year-over-year profit growth look “weak” on paper, even if the core business (product sales) grew by 28% or more. The market is still adjusting to this “higher quality” but “smoother” revenue profile.

댓글 남기기