Alteogen is evolving from a platform provider into a global biopharmaceutical powerhouse. Its strategy is anchored by the Hybrozyme (ALT-B4) platform, which is currently the only global competitor to Halozyme’s technology, alongside a high-value biosimilar and ADC pipeline.

1. Hybrozyme (ALT-B4): The SC Conversion Engine

Alteogen’s core moat is Hybrozyme, a proprietary human recombinant hyaluronidase enzyme that enables the subcutaneous (SC) administration of high-volume intravenous (IV) drugs.

- The Keytruda Milestone: In early 2026, the launch of Keytruda Qurex (SC formulation) by MSD (Merck) served as the ultimate commercial validation. The assignment of the J-code in April 2026 is expected to accelerate insurance reimbursement and market penetration.

- Strategic Flexibility: Unlike competitors, Alteogen provides non-exclusive rights for specific targets (excluding Keytruda), allowing for a broader “multi-partner” strategy that maximizes royalty streams from various biologics and ADCs.

2. ADC-SC: The Next Frontier of Delivery

Alteogen is pioneering the SC formulation of Antibody-Drug Conjugates (ADCs), a segment previously thought to be restricted to IV due to toxicity and molecular complexity.

- Enhertu (SC) Collaboration: Through its partnership with Daiichi Sankyo, ALT-B4 is being applied to Enhertu. Clinical trials in the U.S. and Asia are demonstrating that SC delivery can maintain efficacy while potentially reducing systemic infusion-related reactions.

- Market Disruption: As the ADC market shifts toward outpatient convenience, Alteogen’s platform is becoming the “standard equipment” for next-gen oncology treatments.

3. Specialty Biosimilars & Terugase

Beyond platforms, Alteogen is building a robust portfolio of “Bio-betters” and specialty products.

- Terugase (ALT-BB4): This is Alteogen’s own recombinant hyaluronidase product used to prevent swelling and pain during surgery or to increase the absorption of other injected drugs. It represents the company’s first step into direct commercial manufacturing.

- Eyleaxvi (ALT-L2): An Eylea biosimilar that recently received European Commission (EC) marketing authorization. By combining this with its SC technology, Alteogen is creating a “Bio-better” version that offers superior patient convenience.

Valuation Report: Alteogen (2026.02.17)

The “Reality Check” Phase: Adjusting for the 2% Royalty

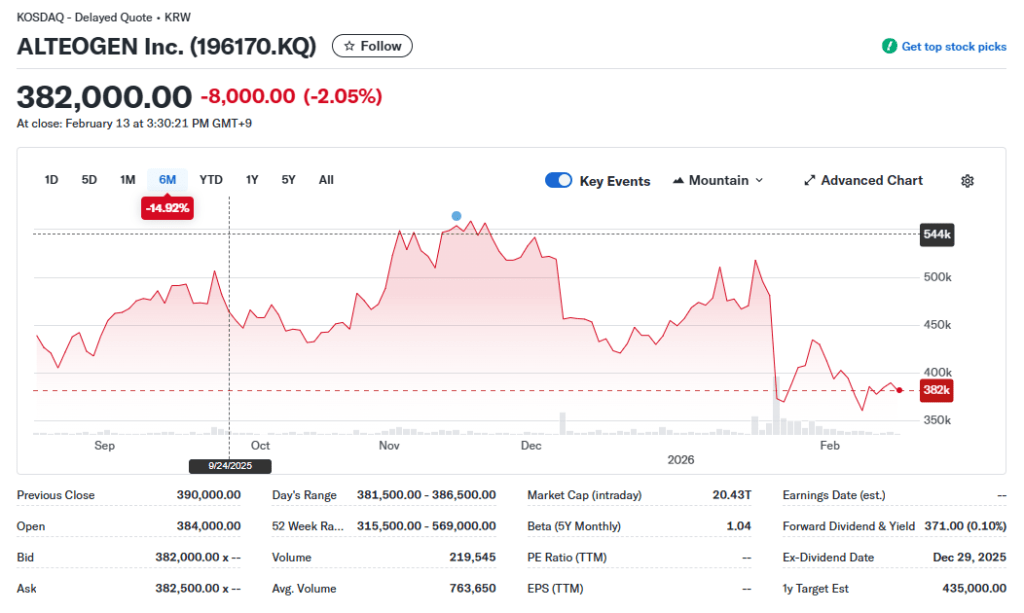

The market cap of Alteogen has faced a significant correction (from KRW 29T to ~20T) as the “Royalty Shock” took hold. The 2% royalty rate confirmed in MSD’s filings is a stark contrast to the 5% previously expected by the market.

1. rNPV Analysis: Sum-of-the-Parts (SOTP) Valuation

Calculated at 1 USD = 1,450 KRW. Success probabilities (PoS) reflect a “Execution Discount” for ongoing litigation.

| Asset / Segment | Type / Status | Est. POS | rNPV Valuation |

| Keytruda SC (ALT-B4) | 2% Royalty / Commercial | 100% | $6.41B (9.30T KRW) |

| Enhertu SC (ALT-B4) | ADC / Ph 2/3 | 40% | $2.41B (3.50T KRW) |

| Additional L/O Deals | GSK, Sandoz, etc. | 30% | $1.17B (1.70T KRW) |

| Eyleaxvi (ALT-L2) | Biosimilar / Approval | 95% | $0.62B (0.90T KRW) |

| Terugase / Assets | Cash & Own Products | 100% | $0.41B (0.60T KRW) |

| Total Pipeline Value | $11.02B (16.00T KRW) |

2. Financial Performance & Peer Multiples

- Market Correction: The total implied value has been revised down to 16.0T KRW, reflecting the 2% royalty reality and a 20% risk buffer for the Halozyme litigation.

- EV/EBITDA Re-rating: Alteogen’s multiple is contracting from a “growth biotech” 40x to a “royalty platform” 20x-25x, closer to Halozyme’s historical trading range.

| Company | Platform Status | Market Cap (USD) | Market Cap (KRW) |

| Halozyme | Commercial (Proven) | ~$8.4B | ~12.2T KRW |

| Alteogen | Commercial (Transitioning) | ~$14.1B | ~20.4T KRW |

3. Why the “Premium” is Justified (Even with Risks)

- Unparalleled Volume: Keytruda is a $30B+ blockbuster. Even at 2%, the sheer volume of sales provides a reliable long-term cash cow that few biotechs can match.

- The “Lilly-Standard” Era: Alteogen’s role in extending patent life for Big Pharma (Evergreening) ensures that its technology remains an essential strategic tool, regardless of the royalty rate.

Strategic Conclusion

- Current Status: Entering a “Show-Me” story phase where actual royalty checks must replace speculative expectations.

- Investment Verdict: Accumulate on Conservative Re-rating

Alteogen remains a fundamental leader in the SC transformation space. However, with the 2% royalty confirmed and Halozyme litigation ongoing, the 20T KRW market cap is no longer a “cheap” entry point. Investors should target an entry around the 15T ~ 16T KRW range as the fair value floor, while treating the J-code launch in April 2026 as the next significant catalyst for trust recovery.

Market Snapshot [2026.02.13]:

While the market now views Alteogen as a “cash-generating platform” rather than a mere biotech venture, the following four downside risks must be carefully weighed by any conservative investor.

A quick reality check on the risks:

1. The “Royalty Shock”: Gap Between Expectation (5%) and Reality (2%)

The most significant headwind for Alteogen’s valuation is the finalized royalty structure for its flagship asset.

- Market Assumption: Historically, investors estimated a 5–8% royalty rate based on global peer Halozyme’s precedents.

- The Reality: As of early 2026, MSD (Merck) filings confirmed the royalty rate for Keytruda SC (QLEX) is set at 2%.

- Impact: Even with a high conversion rate (e.g., 50% of the $30B Keytruda market), a 2% royalty yields roughly 430 billion KRW annually—less than half of the 1 trillion KRW originally anticipated. This “Royalty Gap” forces a downward revision of the long-term cash flow models.

2. Litigation Noise: Halozyme’s Strategic Offensive

Alteogen is no longer flying under the radar; it is now in a direct legal confrontation with the industry incumbent, Halozyme Therapeutics.

- Injunction Risks: In late 2025, Halozyme secured a preliminary injunction (PI) in Germany, temporarily complicating the European launch of Keytruda SC. While appeals are ongoing, this creates immediate uncertainty in the 2026 revenue timeline.

- Patent Validity (IPR): Halozyme has filed an Inter Partes Review (IPR) in the U.S. against Alteogen’s manufacturing patents. Although Alteogen’s core substance patent for ALT-B4 remains valid until 2043, any loss in manufacturing patent protection could invite biosimilar competition or force costly legal settlements.

3. Valuation Premium vs. Global Peers (Halozyme)

When compared to its primary global competitor, Alteogen’s current valuation carries a significant premium that may be difficult to sustain without constant “new deal” news.

- Halozyme (HALO): Trades at a relatively stable 16x–20x P/E ratio as a mature, cash-positive entity.

- Alteogen (196170): Its market cap exceeds 22 trillion KRW, trading at a significantly higher forward multiple. This implies that the market is not just pricing in Keytruda, but also the guaranteed success of future ADC (Antibody-Drug Conjugate) and subcutaneous (SC) conversions that have yet to reach the commercial stage.

4. The “Internalization” Trend Among Big Pharma

While Alteogen’s Hybrozyme is currently the only viable alternative to Halozyme, the long-term threat is internal technology development.

- Case Study: Companies like Celltrion have already demonstrated that high-concentration formulations can sometimes bypass the need for hyaluronidase enzymes (as seen with Zymfentra).

- Future Threat: If Big Pharma successfully develops internal “bio-better” technologies or high-concentration delivery systems to avoid paying permanent royalties (2% or otherwise), Alteogen’s addressable market for new contracts could shrink, turning it into a “one-hit wonder” tied primarily to the Keytruda lifecycle.

Technical Analysis: The “Hyaluronidase” Risk Assessment

Alteogen is currently a market leader in the SC transformation space, but a long-term (5-10 year) view reveals significant structural threats that could erode its platform premium.

1. The Threat of “Internalization” & High-Concentration Tech

- The Celltrion Precedent: The success of Celltrion’s Zymfentra has proven that high-concentration formulation technology can achieve SC administration without hyaluronidase enzymes. If Big Pharma replicates this “bio-better” approach, Alteogen’s platform may be bypassed to avoid permanent royalty payments.

- Next-Gen “Particulation” Tech: Emerging startups like Inventage Lab (JPM 2026) are introducing “biofluidic particulation.” This technology reduces the volume of antibodies into highly concentrated particles, aiming for 3mL injections without needing to “open tissue space” via enzymes.

2. Potential for Superior Patents (The “Legacy Technology” Risk)

- Beyond Hyaluronidase: Within 10 years, the current method of “digesting skin tissue” may be viewed as primitive. Next-gen drug delivery systems (DDS), such as pain-free microneedles or nano-encapsulated controlled release, could offer superior safety and patient compliance, rendering Alteogen’s ALT-B4 a “legacy” technology.

3. Litigation Reality: Not Just “Noise”

- Halozyme’s Global Offensive: The IPR (Inter Partes Review) filed by Halozyme in the U.S. and the Preliminary Injunction in Germany (Dec 2025) are strategic hurdles that could delay commercial launches or force Alteogen into profit-sharing settlements, significantly impacting the “pure royalty” model.

Valuation Report: Alteogen (The Conservative Bear Case)

The “Royalty Shock” Reality Check

The recent confirmation via MSD’s SEC filings that the royalty rate is 2%—not the 5-8% previously hyped by the market—requires a drastic re-rating of Alteogen’s fair value.

1. rNPV Analysis: Bear Case Scenario (Fair Value: ~13.5T KRW)

Calculated at 1 USD = 1,450 KRW. Applying a 30% “Execution & Litigation Discount” to account for legal uncertainty.

| Asset / Segment | Type / Status | Est. POS | rNPV (Conservative) |

| Keytruda SC (ALT-B4) | 2% Royalty / Commercial | 100% | $5.17B (7.50T KRW) |

| Enhertu SC (ALT-B4) | ADC / Ph 2/3 | 35% | $1.72B (2.50T KRW) |

| Other L/O Deals | GSK, Sandoz, etc. | 25% | $0.83B (1.20T KRW) |

| Biosimilars & Cash | ALT-L2 & Cash | 90% | $0.89B (1.30T KRW) |

| Asset Adjusted Total | $8.61B (12.50T KRW) | ||

| + Platform Option Value | Future Tech Potential | – | $0.69B (1.00T KRW) |

| Revised Fair Value | $9.30B (13.50T KRW) |

- Rationale: We assume a lower 40% IV-to-SC conversion rate for Keytruda (vs. the optimistic 50-60%) and include significant legal reserves for the ongoing patent war with Halozyme.

2. Peer Comparison & Market Multiples (The Overvaluation Gap)

As of Feb 2026, Alteogen’s market cap (approx. 20.4T KRW) is nearly 1.6x higher than its global peer, Halozyme, despite Halozyme having a more mature commercial portfolio.

| Company | Commercial Status | Market Cap (KRW) | Valuation Status |

| Halozyme | 5+ Approved Products | ~12.2T KRW | Industry Benchmark |

| Alteogen | Transitioning / High Risk | ~20.4T KRW | Premium Over-extended |

Strategic Conclusion: “Show Me the Money” Phase

- Investment Verdict: Underperform / Wait-and-See

Alteogen’s current 20T KRW+ valuation is built on a “Perfect Execution” scenario where every lawsuit is won and every drug successfully switches to SC. However, the 2% royalty reality and rising technical competition suggest that the “easy money” has already been made.

- Immediate Downside: If the German appeal fails or the U.S. IPR results in June 2026 are unfavorable, a correction toward the 13T – 15T KRW range (the Halozyme floor) is highly likely.

- Long-term Outlook: The emergence of “biofluidic particulation” and Big Pharma’s internal R&D could shorten the commercial lifespan of hyaluronidase-based platforms.

Final Verdict: “Fair value is conservatively estimated at 13.5T KRW. The current market price represents an overheated segment driven by momentum. Investors should wait for the April 2026 J-code assignment and actual royalty data before considering a new entry.”

댓글 남기기